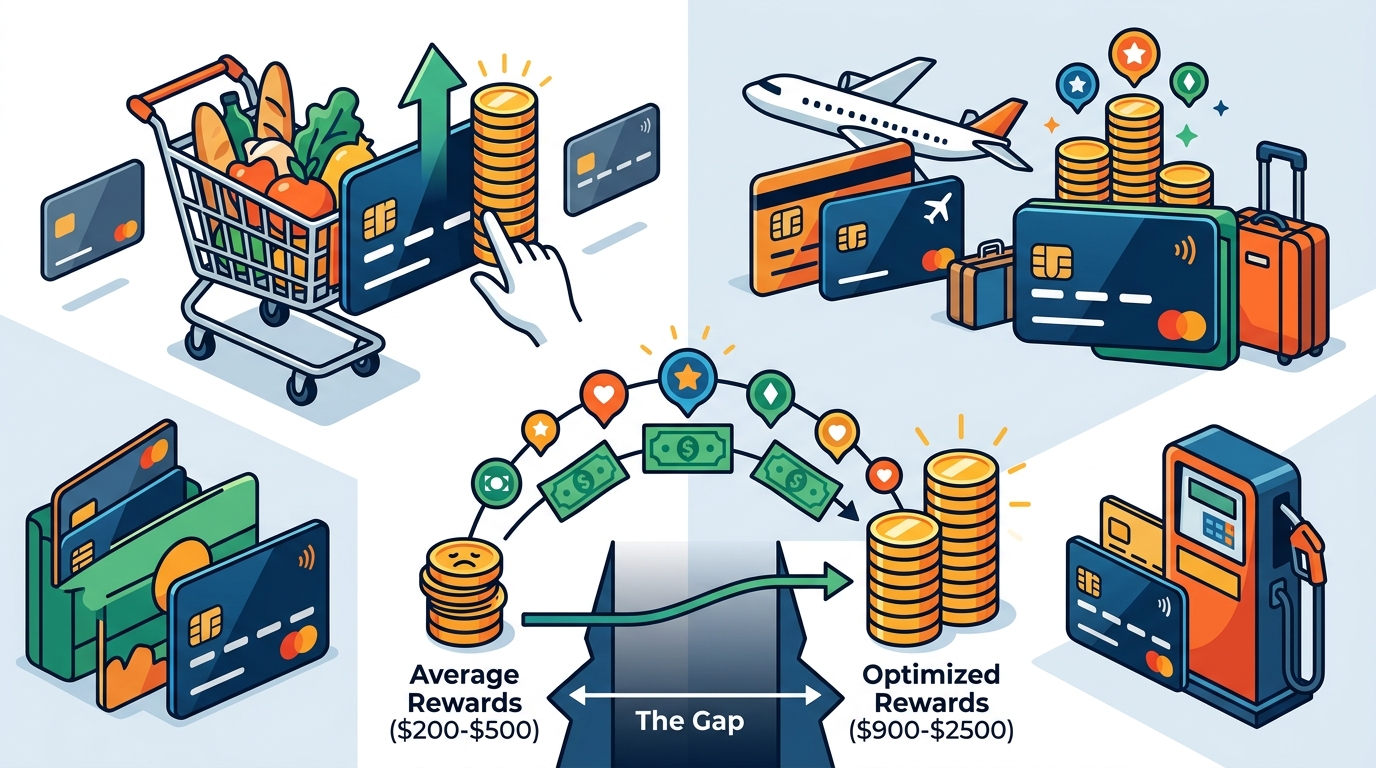

Most Americans earn far less from their credit cards than they could. The average credit card user takes home just $200 to $500 per year in rewards, yet households spending $60,000 annually can unlock $900 to $2,500 simply by using the right card for each purchase. The gap between those two numbers is real money you are leaving on the table every single swipe. This guide breaks down exactly where that lost value hides, how optimization closes the gap, and what tools like savvX do to automate the entire process for you.

The Rewards Gap: What Most People Leave Behind

Credit card rewards optimization is the practice of matching each purchase to the card in your wallet that earns the highest return for that specific merchant or spending category. It sounds simple, but most cardholders never do it.

According to CFPB data reported by The Motley Fool, Americans earned $47 billion in credit card rewards in 2024 but redeemed only $43 billion, with 2.8% of rewards forfeited in Q4 alone. The average rewards balance at year-end was just $192. That means billions of dollars in earned value simply evaporate.

The difference between a passive cardholder and a strategic one can easily amount to $500 or more each year, according to PFCU's 2026 rewards guide. For higher spenders, the gap widens dramatically.

Where Hidden Value Hides in Your Wallet

Unrealized value typically sits in three places: mismatched cards, unclaimed statement credits, and low-value redemptions.

Mismatched Cards

Using a flat 2% cash-back card at the grocery store when you hold a card earning 6% on supermarkets costs you 4 cents on every dollar. On $6,000 in annual grocery spending, that is $240 left behind. The savvX card catalog tracks 343 cards and 130+ transfer partners to surface exactly these mismatches.

Unclaimed Credits

Premium cards often bundle $200 to $300 in annual statement credits for dining, travel, or streaming. Many cardholders forget to activate or use them before the benefit year resets, effectively paying a higher net annual fee than necessary.

Low-Value Redemptions

The baseline value of most credit card points hovers around 1 cent each, but redemption values can range from 0.5 cents to over 2 cents per point depending on the method. Redeeming through airline transfer partners for premium-cabin awards often yields the highest per-point value. savvX's subscription model exists specifically to help you find those high-value redemption paths without bias.

The Optimization Math: Flat-Rate vs. Category Strategy

A spending optimization strategy is an approach that assigns every purchase to the highest-earning card in your wallet based on merchant category codes. Here is how the math compares for a household spending $60,000 per year:

| Strategy | Effective Rate | Annual Rewards | Difference vs. Flat 1.5% |

|---|---|---|---|

| Single flat-rate card (1.5%) | 1.5% | $900 | -- |

| Single flat-rate card (2%) | 2.0% | $1,200 | +$300 |

| Two-card category stack | 2.5% | $1,500 | +$600 |

| Full wallet optimization (4-5 cards) | 3.5%-4.0% | $2,100-$2,400 | +$1,200-$1,500 |

Moving from a single flat-rate card to a fully optimized wallet can add $1,200 to $1,500 in annual rewards. That figure aligns with industry benchmarks showing optimized users save roughly $1,200 per year just by swiping the right card at the right time.

Sign-Up Bonuses: The Biggest Single Lever

A sign-up bonus (also called a welcome bonus) is a one-time reward a card issuer offers new cardholders who meet a minimum spending requirement within a set period, typically three months. These bonuses range from $200 to over $1,000 in value and represent the single largest reward opportunity in any given year.

Missing a single $750 welcome bonus is equivalent to losing years of ongoing cash-back earnings. savvX tracks your progress toward each bonus threshold so you never fall short by a few dollars.

Timing matters: align bonus spending requirements with planned large expenses like insurance premiums, tax payments, or home repairs you would make anyway. Never spend extra just to hit a threshold.

The Annual-Fee Trap (and How to Beat It)

An annual fee is a yearly charge a card issuer levies for account membership, typically ranging from $95 to $695 for premium rewards cards. The fee is only a trap when the card's net value to you turns negative.

The formula is straightforward: Net Value = (Annual Spend x Effective Reward Rate) + Credits + Perks Value - Annual Fee. If a card charges $550 but delivers $300 in statement credits, $200 in lounge-access value, and $400 in bonus-category rewards, its net value is +$350. If your spending patterns change and those numbers drop, it is time to downgrade.

savvX continuously re-evaluates net card value against your real transactions and alerts you when a card no longer pays for itself, so you can downgrade or cancel before the next fee posts.

Why Automation Beats Spreadsheets

Manually tracking rotating categories across five cards, monitoring bonus progress, and calculating per-point redemption values is a part-time job. Most people start strong and then default to a single card within weeks.

Automated optimization tools connect to your accounts via read-only bank feeds (savvX uses Plaid for secure access) and do the matching instantly. The key differentiator is the business model behind the recommendation. Services funded by affiliate commissions or card-issuer partnerships have a financial incentive to recommend the card that pays them the highest referral fee, not the card that earns you the most.

savvX charges a subscription fee as its only revenue source, which means every recommendation is optimized for your rewards math, not a referral payout. That alignment is what turns a helpful tool into a trustworthy advisor.

Key Takeaways

- The average cardholder earns $200-$500 per year in rewards; optimized cardholders can earn $1,200-$2,500 on the same spending.

- Mismatched cards, unclaimed credits, and poor redemption choices are the three biggest sources of lost value.

- A full wallet-optimization strategy with 4-5 cards can boost your effective rewards rate from 1.5% to 3.5%-4%.

- Welcome bonuses are the single largest reward lever, often worth $500-$1,000+ in a single quarter.

- Annual fees are only worth paying when net card value stays positive after accounting for credits and perks.

- Automation eliminates the manual tracking burden that causes most optimization strategies to fail.

- Subscription-only business models (like savvX) remove affiliate bias from card recommendations.

Frequently Asked Questions

How much can the average person save by optimizing credit cards?

A household spending $60,000 per year can typically increase annual rewards from around $900 (single flat-rate card) to $2,100 or more with a multi-card strategy. That is an extra $1,200 per year without changing what you buy.

Is credit card optimization worth it if I only have two cards?

Yes. Even moving from one flat-rate card to a two-card stack (one category card plus one flat-rate) can add $300-$600 in annual rewards on moderate spending.

Do I need to carry a balance to earn more rewards?

No. Carrying a balance is the fastest way to destroy reward value. With average APRs above 21%, a $5,000 balance costs roughly $1,050 in annual interest, far exceeding any rewards earned on that spending.

What is a credit card rewards optimizer?

A credit card rewards optimizer is a tool or service that analyzes your real spending patterns and tells you which card in your wallet to use for each purchase to maximize your total rewards earnings.

How does savvX differ from free credit card recommendation sites?

savvX earns revenue exclusively from user subscriptions. It does not accept affiliate commissions, card-issuer payments, or advertising revenue. This means its recommendations are driven entirely by your rewards math, not by which card pays the platform the most.

Are sign-up bonuses really that valuable?

Welcome bonuses range from $200 to $1,000 or more. A single missed $750 bonus can equal years of ongoing cash-back earnings from everyday spending.

Will connecting my bank accounts to savvX compromise my data?

savvX connects through Plaid, which provides read-only access to transaction data. savvX cannot move money, make charges, or sell your data. Its privacy policy is available at savvx.com/privacy.

When should I cancel or downgrade a premium credit card?

Cancel or downgrade when the card's net value turns negative, meaning the annual fee exceeds the combined value of rewards earned, credits used, and perks consumed. savvX monitors this automatically and sends alerts before your next fee posts.

Start Seeing What You Are Missing

Every swipe on the wrong card is money you will never get back. Try savvX today to see exactly how much more your current spending could earn, with zero affiliate bias and recommendations built solely around your wallet.